Pip: Nkozi Knight writes about the economy the way a doctor reads an X-ray — calmly, and with bad news.

Mara: This episode covers two territories: the financial pressures quietly reshaping ordinary Americans' retirement savings and debt load, and the cultural forces eroding the attention and civic seriousness needed to even notice. Let's start with the money.

Debt And Financial Fragility

Mara: The question underneath these posts is who actually absorbs the risk when large financial systems reprice — and whether ordinary workers ever consented to the role they've been assigned.

Pip: The 401(k) post puts it plainly. Setting up the core mechanism, the post reads: "Wall Street creates the paper value in private markets, waits until the valuation becomes too large for traditional buyers to absorb, changes the rules so these companies can enter major indexes faster, and then lets passive retirement money like your pension become the final buyer."

Mara: So the upshot is: the worker never voted on any of this. The money moves because index methodology says it moves — payroll deductions, automatically, every two weeks.

Pip: And the Nasdaq rule change from May 2026 is the mechanism. Newly public companies can now enter the Nasdaq 100 after just fifteen trading days. That's not a technical footnote — that's a faster on-ramp for private insiders to reach public exit liquidity.

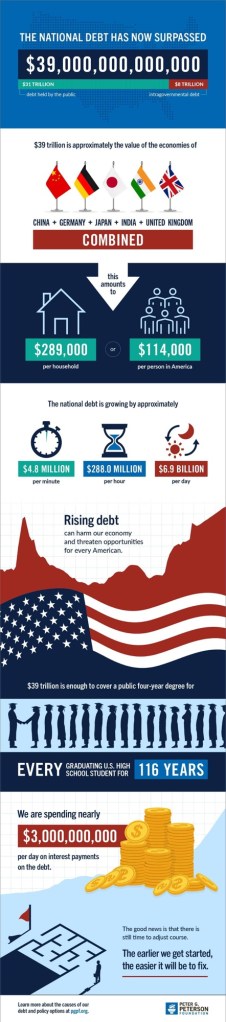

Mara: The sovereign debt post widens the frame. Nearly thirty-nine trillion dollars in federal debt, deficits approaching two trillion annually, and the government now spending roughly one trillion dollars a year just on interest — not defense, not infrastructure, just servicing prior obligations.

Pip: And the piece on everyday economic stability makes the lived version of that math visible: families paying more for gas, groceries, insurance, and travel while the stock market's recovery runs on a handful of AI-adjacent names. A 401(k) can show green while the household budget turns red.

Mara: That's the split-screen economy — and it connects directly to who's being asked to fund what comes next.

Attention And Civic Culture

Pip: If the financial posts describe a system that depends on passive money, this segment asks whether the culture has become too distracted to push back on anything.

Mara: The War on Thinking frames the problem directly: "As information has become more accessible, independent thought appears to have become more difficult." The post argues that the threat to critical thinking isn't censorship — it's abundance, and the economic incentives that reward reaction over reflection.

Pip: Algorithms don't monetize pausing. The person who investigates a claim before sharing it is, by the platform's logic, a worse user than the one who amplifies instantly.

Mara: And that pattern, the post notes, runs well beyond politics — into how people invest, how they evaluate financial narratives, how they form any judgment at all. The amateur says the answer is obvious; the expert says it depends. Engagement rewards the former.

Pip: Which is a fairly brutal diagnosis for a moment when people most need to be asking hard questions about, say, whose money is financing the AI buildout.

Mara: The Michelle Obama Day post approaches civic culture from a different angle — not information overload, but what happens when a lifetime of documented public achievement gets answered with dehumanization. The post's argument is that the attack is rarely on the accomplishment itself; it's on the legitimacy of the person who accomplished it.

Pip: And that pattern, the post notes, has a long history in how Black excellence gets received in America.

Mara: Both posts are really asking the same underlying question: what kind of public culture do you need to hold systems accountable — and whether we're building toward that or away from it.

Pip: Paper wealth, automatic money, distracted citizens — it's a fairly coherent picture of how a system stays invisible to the people inside it.

Mara: Next time, we'll see what else is on the site. The questions here don't resolve quickly.