By Nkozi Knight

The most important economic story in America is not the stock market.

It is not Bitcoin.

It is not artificial intelligence.

It is not even inflation.

It is debt.

More specifically, it is what happens when the world’s largest economy accumulates nearly $39 trillion in debt while simultaneously asking investors to continue financing deficits approaching $2 trillion a year.

That number is so large it becomes difficult to comprehend.

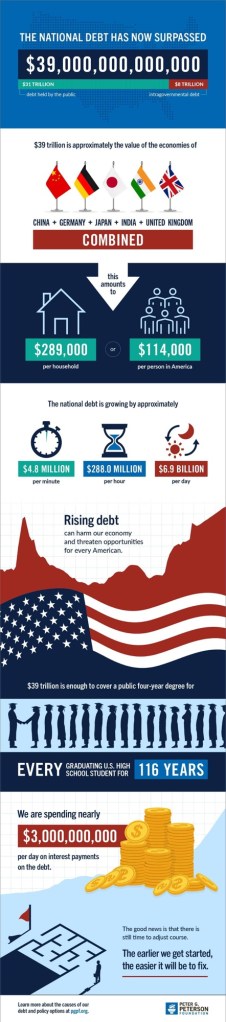

Broken down across the population, America’s debt burden now exceeds roughly $114,000 for every person in the country.

A family of four is effectively carrying more than $450,000 of federal debt.

No, the government is not sending anyone a bill.

But that does not mean the debt disappears.

Someone always pays.

The question is how.

For decades, the answer was simple.

The United States occupied a unique position in the global economy. The dollar served as the world’s reserve currency, global commerce flowed through dollar-based financial systems, and foreign governments accumulated Treasury securities as reserves.

America benefited enormously from this arrangement.

We could borrow more, spend more, run larger deficits, and face fewer consequences than any other nation in history.

The system worked because the rest of the world trusted American debt.

Today that trust is beginning to show signs of strain.

The warning signs are not coming from politicians.

They are coming from the bond market.

The yield on the 30-year Treasury bond has climbed to around 5 percent, levels not seen consistently since before the financial crisis.

That number matters far more than most people realize.

A Treasury yield is not simply an interest rate.

It is a measure of confidence.

When investors believe the future is stable, they accept lower returns.

When risks increase, they demand higher compensation.

A 5% 30-year Treasury bond is the market’s way of saying the old assumptions are no longer enough.

And the timing could not be worse.

The federal government is projected to spend approximately $1 trillion this year just servicing existing debt.

$1 TRILLION dollars spent not on defense, infrastructure, education, veterans, or health care, but on interest.

Nothing productive is created.

The money simply services obligations accumulated in previous years.

As debt grows, those interest costs grow with it.

And because much of America’s debt was issued when rates were near zero, older bonds must eventually be refinanced at today’s much higher rates.

The result is simple math.

More debt.

Higher rates.

Higher interest costs.

Even more debt.

That is how debt spirals begin.

The international picture makes the situation even more concerning.

For decades, countries such as Japan and China helped finance America’s borrowing because Treasury bonds were considered safe, liquid, and reliable.

But that equation is changing.

Japan’s own debt exceeds twice the size of its economy, and rising domestic yields now give investors meaningful returns at home. China has also been reducing Treasury holdings while diversifying trade and reserve assets.

Neither country is abandoning the United States.

That misses the point.

The issue is marginal demand.

When the largest buyers purchase less, somebody else must step in.

To attract those buyers, yields must rise.

Higher yields mean higher borrowing costs that eventually flow through the entire economy.

Mortgage rates rise.

Auto loans rise.

Credit card rates rise.

Business financing becomes more expensive.

Commercial real estate becomes harder to refinance.

Economic growth slows.

At the same time, inflation remains stubbornly elevated.

Energy prices have surged.

Producer prices continue moving higher.

Supply chains remain vulnerable to geopolitical shocks.

Because energy sits at the center of transportation, manufacturing, and logistics, higher fuel costs ripple through the entire economy.

Consumers experience this reality every day.

Groceries cost more.

Insurance costs more.

Travel costs more.

Housing costs more.

The official inflation number may be one statistic, but the lived experience often feels much higher.

This is where the debt story and inflation story merge.

The government has very few attractive options.

It can cut spending.

It can raise taxes.

It can accept slower growth.

Or it can continue borrowing and creating additional liquidity.

Historically, heavily indebted governments tend to choose the path that appears least painful in the short term.

More borrowing.

More debt issuance.

More intervention.

More money creation.

The danger is not an immediate collapse.

That is what many people get wrong.

The United States is not likely to wake up one morning and discover that Treasury bonds are worthless or that the dollar has suddenly disappeared.

Financial systems rarely fail that way.

Confidence erodes gradually.

Then suddenly.

The greater risk is a slow deterioration in purchasing power, combined with rising interest costs and weakening demand for American debt.

The petrodollar system is not disappearing tomorrow, but it is facing challenges that would have been unthinkable twenty years ago. More nations are settling trade in alternative currencies. Regional trading blocs are reducing dependence on the dollar. Central banks are diversifying reserves.

The dollar remains dominant.

But dominance is not permanence.

And that distinction matters.

Because America’s extraordinary borrowing power has always depended on extraordinary global demand for dollars and Treasury securities.

If that demand weakens, even modestly, the math changes.

And once the math changes, the bond market notices.

The bond market is noticing now.

The question is whether Washington is paying attention.

Because at some point debt stops being a political issue.

It becomes an arithmetic problem.

And arithmetic does not care about ideology, campaign promises, or election cycles.

Eventually, the numbers win.