The 2026 Iran conflict has delivered more than oil supply shocks and naval blockades, it has spotlighted a disturbing pattern of suspiciously timed trades in oil futures, equities, and prediction markets. In at least three documented episodes, hundreds of millions (and in one case nearly a billion) dollars were wagered on falling oil prices mere minutes before major de-escalation announcements by President Trump or Iranian officials. The precision and scale of these bets have triggered investigations by the Commodity Futures Trading Commission (CFTC), complaints from advocacy groups, and bipartisan scrutiny from Congress.

While markets are supposed to reflect all available information under the efficient-market hypothesis, these events suggest a troubling information asymmetry: a small group of traders appears to have acted with foreknowledge of policy shifts that directly moved energy prices. This is not abstract market theory. It raises core questions about market integrity, the misuse of nonpublic government information, and the regulatory gaps exposed when geopolitics collides with high-stakes derivatives trading.

The Pattern: Three Strikes, Same Playbook

Consider the timeline, drawn from Bloomberg, Reuters, NPR, and Financial Times reporting:

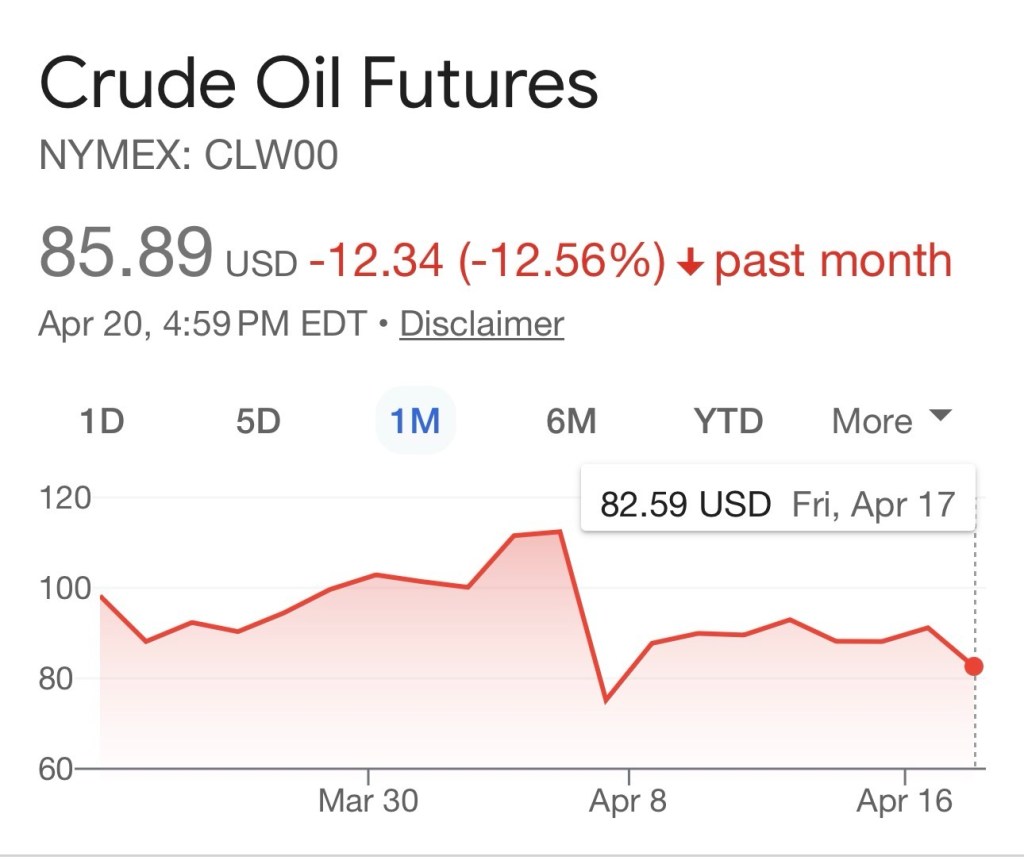

• March 23, 2026: Roughly 15 minutes before President Trump posted that he would delay planned strikes on Iranian energy infrastructure, traders executed approximately $500–580 million in short positions on oil futures (WTI and Brent). When the announcement hit, crude prices plunged as much as 15%.

• April 7, 2026: Roughly $950 million was bet on falling oil prices hours before the U.S. and Iran announced a two-week ceasefire. Oil dropped sharply on the news.

• April 17, 2026: About $760 million in oil shorts were placed roughly 20 minutes before Iran’s foreign minister announced the Strait of Hormuz would reopen to commercial traffic. Oil fell as much as 11% intraday.

These are not isolated retail bets. They represent enormous, concentrated positions executed with surgical timing. On prediction markets like Polymarket, similar patterns emerged: one trader reportedly turned $3,200 into $600,000 on a U.S.-Iran ceasefire outcome one hour before it was public; other accounts netted millions across multiple Iran-related events. A crypto-analytics firm identified six “suspected insiders” who collectively made $1.2 million on a single high-profile outcome.

The White House itself recognized the optics. In a March 24 email, it explicitly warned staff against betting on Iran-war-related prediction markets, implicitly acknowledging that nonpublic information was a risk. Senators Elizabeth Warren and Sheldon Whitehouse have publicly questioned whether government insiders are misappropriating material nonpublic information. Public Citizen filed a formal CFTC complaint citing the “statistical impossibility” of such repeated accuracy absent insider knowledge.

Why This Looks Like Insider Trading

Standard market theory holds that prices incorporate information rapidly. Yet these trades consistently preceded public announcements by minutes, precisely the window in which only those “in the know” (administration officials, military planners, or their close associates) would have material nonpublic information.

The mechanics are straightforward:

• De-escalation news (ceasefire, delayed strikes, Hormuz reopening) reliably drives oil prices lower by easing supply fears.

• Shorts placed immediately before such news capture the full price drop with minimal risk.

• The volume of hundreds of millions in minutes, far exceeds normal liquidity and shows coordinated or highly informed positioning.

Defense and energy stocks have also shown volatility tied to the same cycle. The MSCI World Aerospace & Defence Index returned 32% year-to-date through March 2026, outpacing broader markets, while oil futures swung wildly on Hormuz rumors. When policy pivots are telegraphed internally, the incentive to monetize that edge is obvious—and the barrier to entry (futures markets, prediction platforms) is low for sophisticated players.

This is not the first time war has blurred the line between national security and personal profit, but the speed and transparency of modern markets (plus the rise of unregulated-ish prediction platforms) have made the anomalies impossible to ignore. Economists like Paul Krugman have bluntly labeled it “treason in the futures markets.”

Regulatory and Ethical Blind Spots

Prediction markets like Polymarket have exploded in popularity precisely because they allow direct bets on real-world events. Yet they operate in a gray zone: the CFTC has limited jurisdiction, enforcement is slow, and anonymity features can shield bad actors. Traditional futures markets are better regulated, but the CFTC’s probes into the March and April trades have so far yielded little public action, prompting criticism that the agency is “rolling over.”

For elected officials and senior staff, the STOCK Act already prohibits insider trading on nonpublic information, but enforcement has been lax. A bipartisan bill introduced in late March would ban members of Congress and senior federal staff from trading prediction-market contracts tied to policy or political events. It is a necessary start, but broader reforms are needed: real-time trade surveillance for geopolitical flashpoints, mandatory pre-clearance for officials with access to classified briefings, and clearer rules around family members and close associates.

The economic stakes are enormous. The Strait of Hormuz carries roughly 20% of global oil trade. Even temporary closures have spiked prices toward $100/barrel, rippling through inflation, consumer costs, and corporate earnings. When insiders front-run those moves, they privatize gains while the public bears the broader economic pain.

Restoring Trust in Crisis Markets

Geopolitical shocks will continue. The lesson from the 2026 Iran episode is that markets do not self-police when information is asymmetrically distributed along lines of power. Regulators, platforms, and Congress must treat these anomalies with the urgency they deserve, not as conspiracy fodder, but as evidence that the system’s integrity is at risk.

Until credible investigations produce accountability, every perfectly timed oil trade will fuel cynicism. Markets thrive on trust. When that trust erodes because the game is rigged for those “in the know,” the damage extends far beyond any single portfolio and we all lose.